The Tools a Lender Needs After a Loan Starts, Scoped Before You Commit to a Stack

Post-origination gets one line in the plan.

"Budget for a servicing platform. Check the box. Move on."

That line is a trap.

The day the first borrower has the money in their account, the real work starts. And if you didn't scope the tools for it, the problems will find you, one at a time, usually when you're least prepared.

You can map every tool you'll actually need before you fund a single loan. Do it. The cost of missing something only goes up after launch.

Most lenders scope this after it's too late

Two weeks from go-live the engine is running, funding works, the app is in review.

Then someone opens the checklist and sees the blanks.

Where does the borrower pay?

How does an agent handle a dispute?

What happens the morning someone files for bankruptcy?

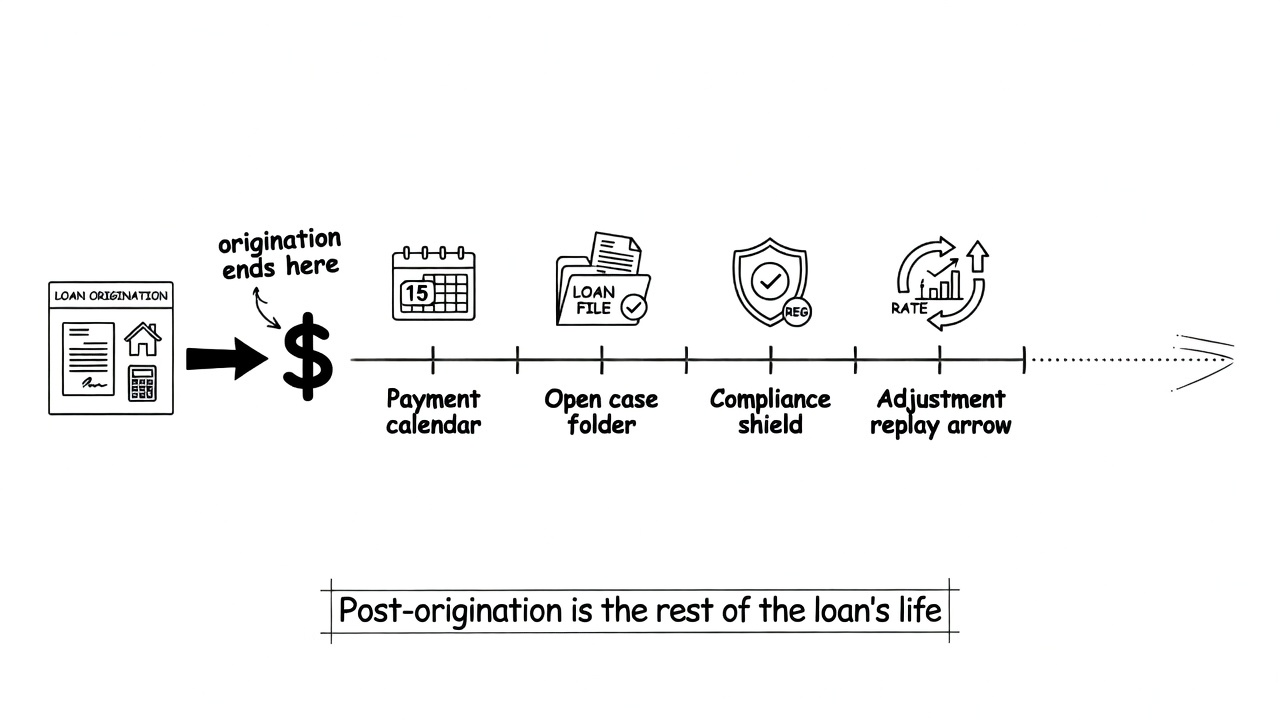

Post-origination is the rest of the loan's life. The cash has already left. What comes next is years of servicing, adjustments, and regulatory events moving across the portfolio at once.

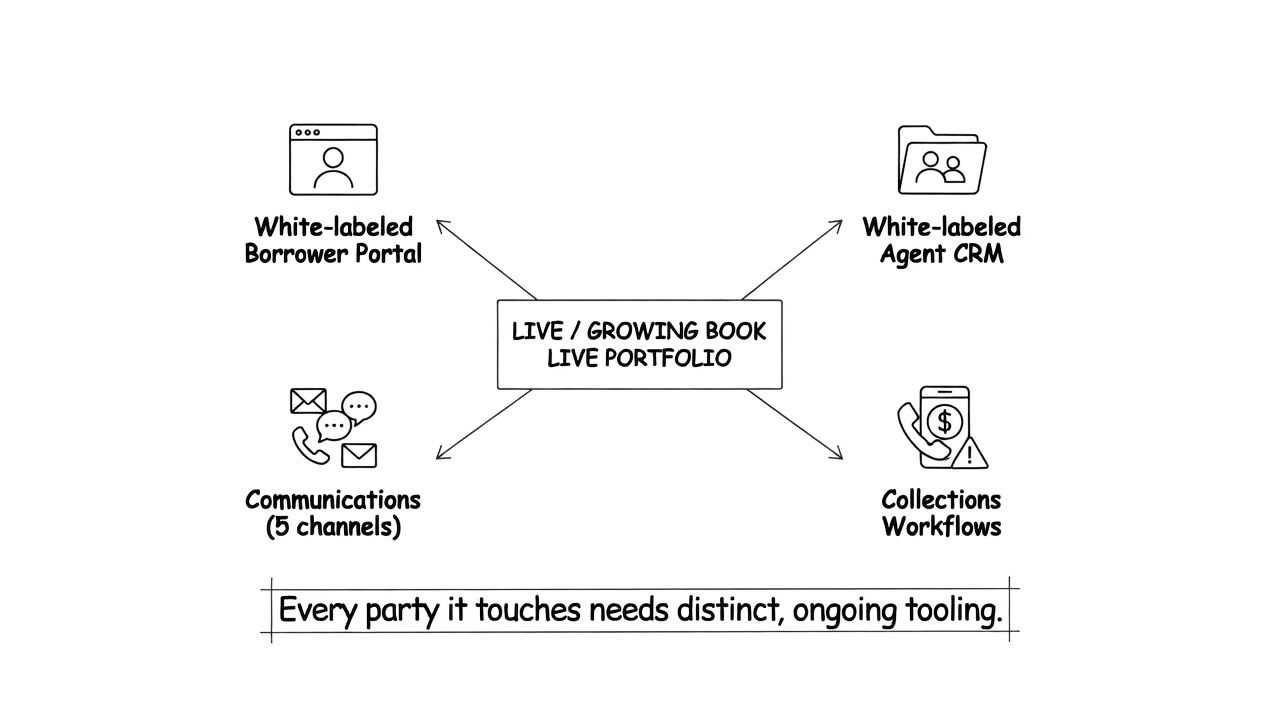

You'll need seven capabilities. None of them come with the origination system.

- A borrower-facing portal for payments and account access

- An agent CRM for servicing and case work

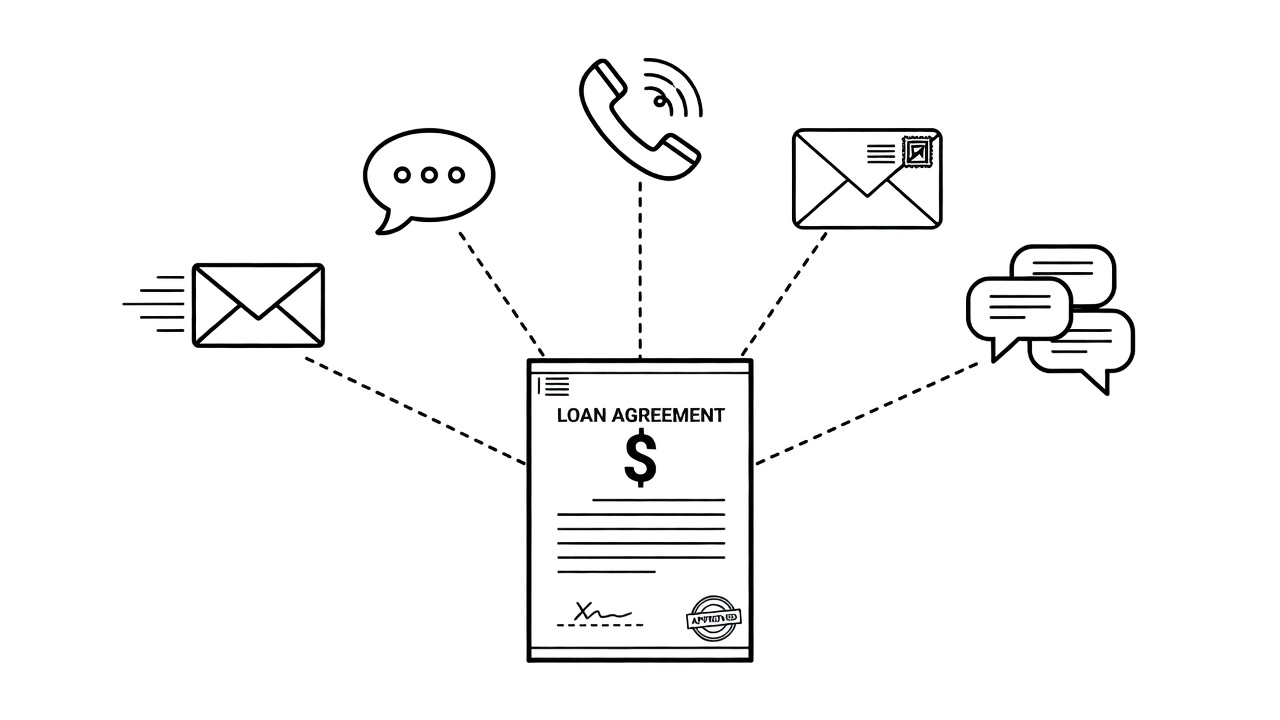

- Multi-channel communications across email, SMS, phone, direct mail, and chat

- Structured case management for the regulated situations that will definitely arrive

- Compliance enforcement that runs before outbound contact goes out

- A retroactive adjustment capability for when a servicing decision was wrong from the start

- Data access methods so the portfolio is visible outside the servicing system

Origination has a finish line. Post-origination doesn't. The moment you fund the first loan, risk starts accumulating on all seven fronts. On thin-margin loans, every manual touch costs more than the loan earns. Your tooling decides how often that happens.

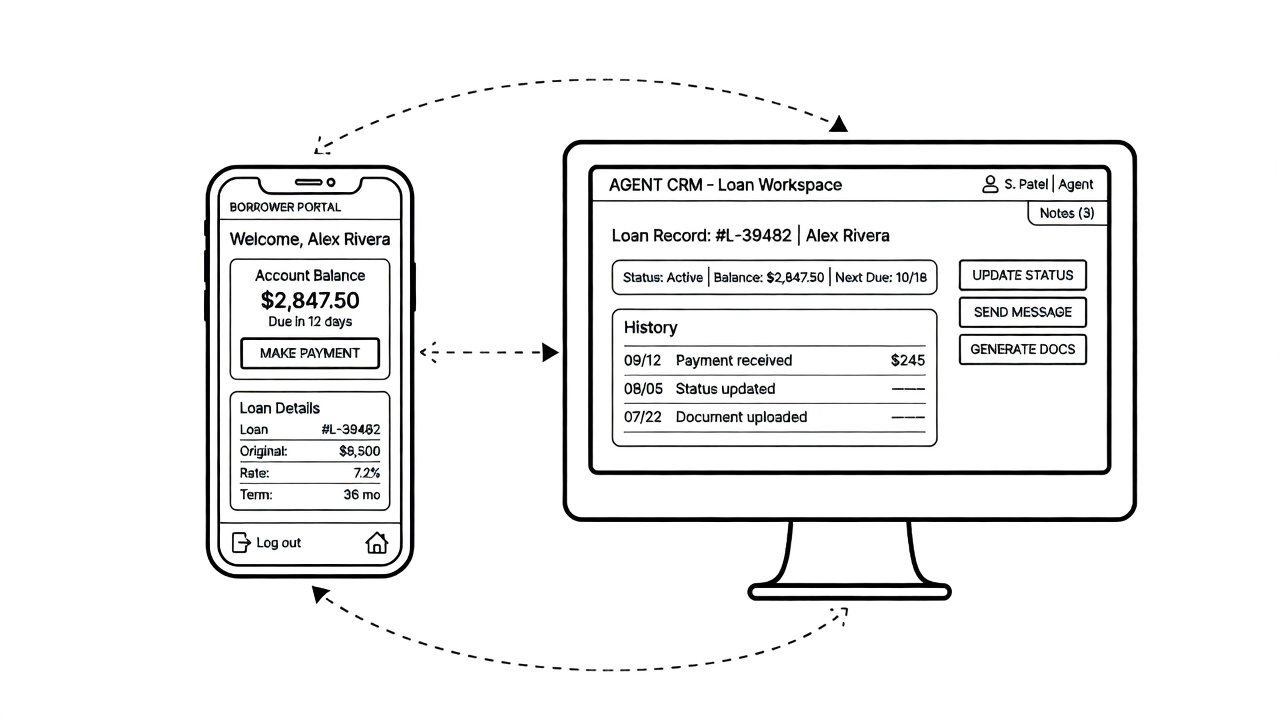

Where the borrower actually lives after funding

A borrower calls. They want to move their payment by five days.

The agent needs to see the full loan state, the history, and the power to make the change right now. Not a read-only screen and a ticket they have to open in another system.

Your agents should work inside a workspace that carries your brand and knows what a loan is. A generic sales CRM will not do this cleanly. You'll end up building bridges you'll have to maintain forever.

The borrower portal has to do the same thing. Your brand. Your data. The ability to act. And it has to keep up as your products evolve. That's not a project you finish once.

Communications gets complicated in a hurry. Five channels. Each one brings its own rules and its own ways to get in trouble.

SMS and calls fall under TCPA and FDCPA. Direct mail has timing rules. Chat adds real-time obligations. Every channel you add is another surface you have to police.

Some borrowers only answer on one channel. The mix you support decides whether you can actually reach the people you need to reach.

Three tools. Three real build-or-buy decisions. The question that follows is the same for all of them: who will own version two when the product changes?

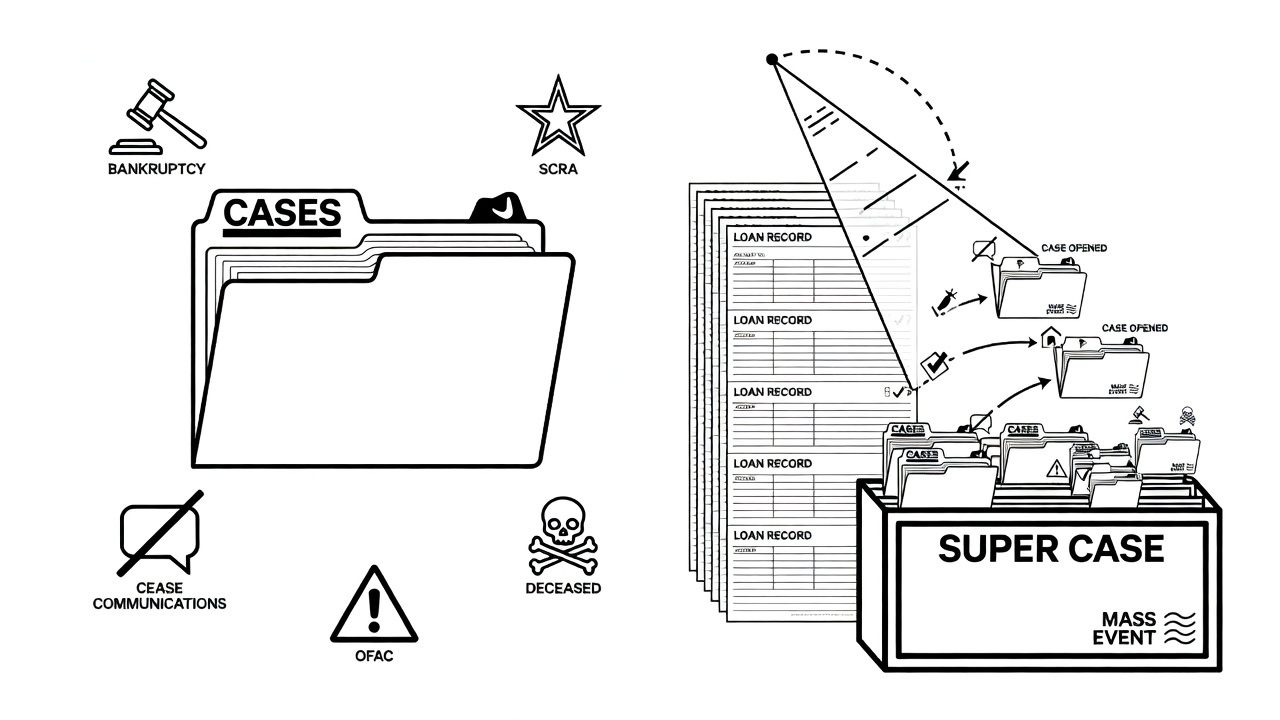

The cases you will get

One of your borrowers gets deployed. Your system doesn't know. For three months it keeps charging the wrong rate. Then the borrower calls. Now you have a compliance problem, no case file, and no record of when the deployment started.

That's not rare. It's completely predictable.

You will see bankruptcy filings. Deaths. OFAC matches. SCRA activations. Disputes. Cease communications requests. Do-not-interact flags. FEMA disasters. Eleven types in total.

Each one carries real legal obligations. None of them can be left to "someone will remember" once the portfolio has any real volume.

The only question that matters is this: does your system catch these before the borrower does?

Auto-detection beats waiting for the phone to ring

Most teams wait for the borrower to call. That works until it doesn't. Until three months go by. Or the filing was two weeks ago and nobody noticed.

Compliance Guard Monitor watches the whole book and opens cases the second it sees the trigger. Before the borrower has to tell you.

For active duty it hits the DoD list and opens the case with the branch and dates already attached. The agent starts with the facts instead of chasing them down.

For bankruptcy it pulls the details from LexisNexis so the team doesn't have to go digging in court records.

For deceased borrowers it attaches the right templates so nobody is drafting from scratch at 10pm.

For OFAC and SDN matches it opens the case immediately.

Every one of these comes with the workflow already built for that exact situation. You don't start from a blank page.

Monitoring is not the same as stopping the bad thing

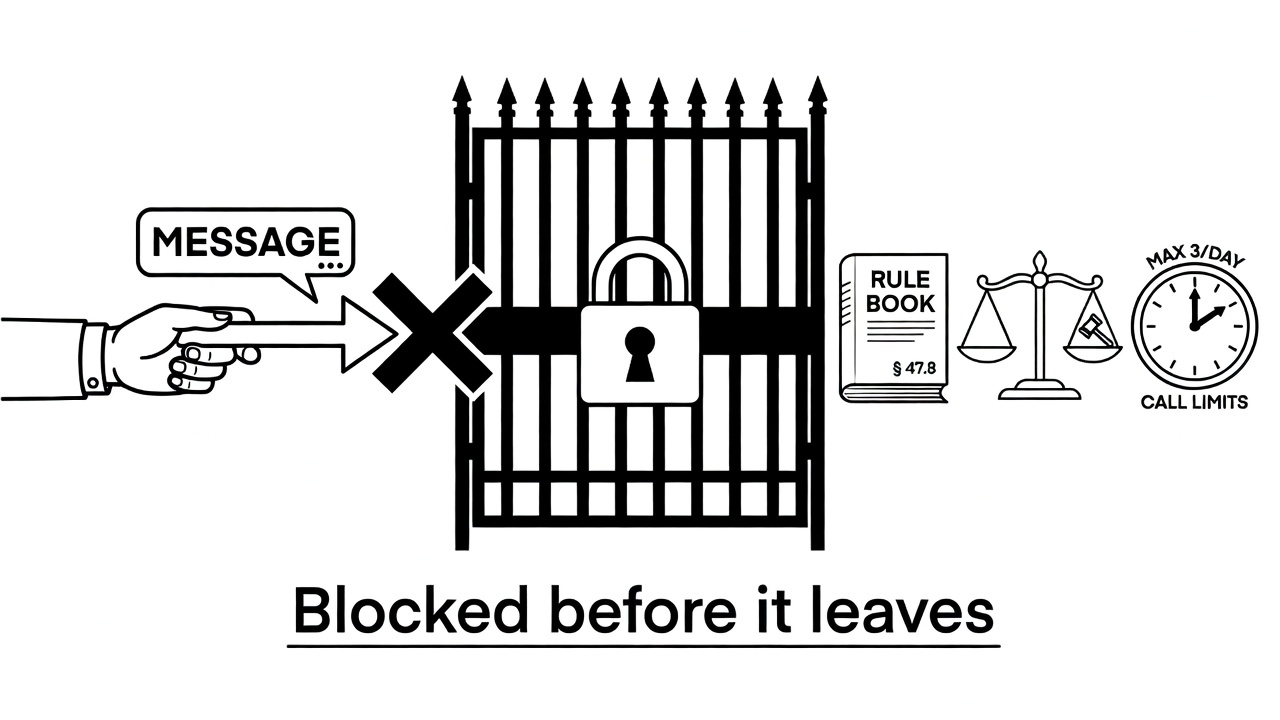

Compliance Guard tracks six frameworks: FDCPA and Regulation F, TCPA, SCRA, UDAP/UDAAP, and the Bankruptcy Code.

Knowing the rules is not the same as enforcing them.

The system blocks non-compliant actions in real time. Agents cannot click through it. If the communication isn't allowed, it simply does not leave.

Massachusetts limits collection calls to two per seven days. The system knows where the borrower stands and stops the third one. The agent doesn't have to keep count. The system does. The obligation doesn't rest on the agent remembering under pressure.

One bad outbound contact can cost five figures under TCPA or FDCPA. The block happens before the message is sent.

When one event hits the whole book at once

A FEMA declaration can affect hundreds of accounts at the same time. Manually opening cases for each one is not a process. It's a backlog waiting to happen.

Super Cases let you apply the same structured workflow across the entire affected group in one move.

A system that only warns is a policy. A system that blocks is enforcement. Policies depend on people not making mistakes when they're busy. Enforcement does not.

When the change happened on the wrong date three months ago

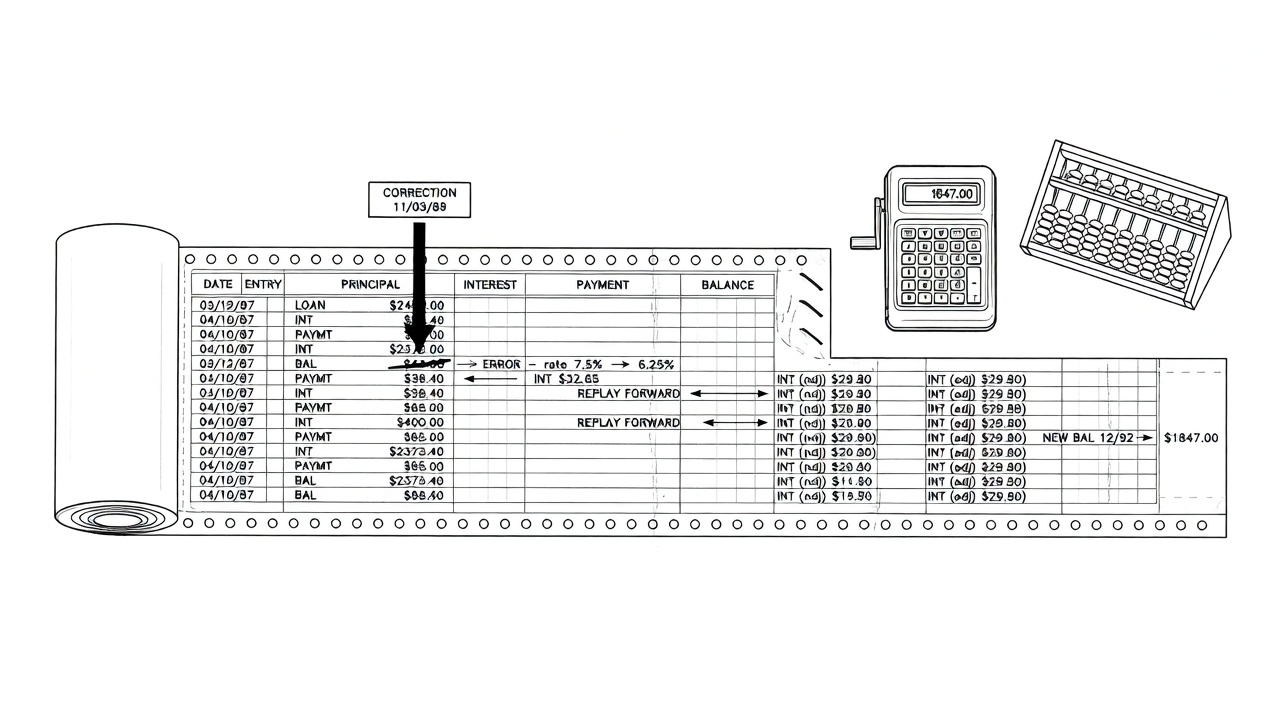

Three months ago a rate modification went in on the wrong effective date. Every statement since has been wrong. Daily interest has been running at the wrong rate the whole time.

The old way: post an adjustment today and try to reconcile everything that happened in between. You end up with a history full of small differences that never quite go away. The original mistake stays in the record.

Loan Replay does it the other way. It puts the correct rate on the correct past date and replays every day since as if that had always been the rule. You get one clean, authoritative history instead of a stack of patches.

Loan Replay is a recalculation engine, not a reconciliation or matching engine. Reconciliation tries to paper over the mistake. Recalculation gives you the record as it should have been.

Not every setting can be changed on a live book. Loan Replay works inside the limits that exist. It recalculates cleanly within those boundaries.

Right now an agent is one click away from sending a collections text to a borrower in Massachusetts who has already taken the two calls allowed this week. Compliance Guard Rules will stop it before it leaves. It checks eligibility and capacity rules before anything leaves. If it fails, the message is blocked. Not sent for review. Blocked.

Voice goes through the same logic because the dialer lives inside the case management tool.

Configuration, support, and getting your data when you actually need it

A lender already running loans wants to change the grace period on an installment product.

Does that mean a sprint, a deploy, and a release window? Or can it go live today?

Peach's Adaptive Core carries more than 200 variables you can change without touching code. Grace periods. Fees. How payments get applied. They go live through configuration.

Not every variable is changeable once loans are live. Some are set at the beginning and stay that way. You need to know which ones matter for your products while you're still implementing, not four months after launch.

When you have a data question, you don't get a help-desk person reading a doc out loud. Peach provides Solutions Engineers on implementation and support calls, not L1 help-desk support. These are real engineers and are not the engineers who wrote Peach's core product code.

Data comes out four ways you control: direct API, webhooks, a database replica you can send to GCS or Snowflake on your own schedule, and loan tapes. You decide the timing.

If every small change requires a deploy and the vendor decides when you can have your own data, you're a tenant. If you can change the rules yourself and pull the data when you need it, you're operating the system.

That difference shows up every single month.

Questions lenders ask when they see the list

A VP Engineering forwards this to the CFO and the compliance lead before a vendor meeting. The CFO wants to know what they're actually buying. The compliance lead wants to know whether the enforcement is real or just nice words. Neither of them is going to read the whole thing. Here are the short answers.

What is the difference between origination and servicing?

Origination ends when the money goes out. Disbursement, KYC, underwriting. Done. Post-origination is everything after that: the portal, the CRM, communications, case management, compliance enforcement, retroactive fixes, and getting your data out. It runs for the entire life of every loan.

Does it actually block bad collections messages, or just warn?

It blocks. Compliance Guard stops non-compliant actions before they happen. Agents cannot override the rule. If it's not allowed, the action does not go through.

What does retroactive adjustment actually do?

Loan Replay applies the correct change on the correct past date and replays the whole period forward. You get one clean history instead of a collection of patches and leftover differences. If the mistake has been running for months, that difference shows up on every statement and every accrual.

What cases does it handle out of the box?

Eleven: bankruptcy, cease communications, debt validation, deceased, dispute, military duty under SCRA, do-not-interact, collections, FEMA, OFAC or SDN, and active duty military. Each one comes with the workflow already built. Super Cases handle events that hit hundreds of accounts at once in a single operation.

How do I get my data out?

Four ways you control: direct API, webhooks, a database replica you can send to GCS or Snowflake on your schedule, and loan tapes.

Can I change configuration without a code deploy?

Yes. More than 200 variables live through configuration. Some structural settings are locked once the portfolio is running. Ask which ones apply to the products you're actually building.

Scope the full surface before you commit

Open the build-vs-buy sheet. Is post-origination actually listed?

Not as a single line that just says "servicing."

As the real surfaces: portal, CRM, communications, case management, compliance enforcement, retroactive adjustment, and data access.

If those aren't scoped before you pick the stack, you'll be scoping them after the first loan funds. That's when the obligations start.

Bankruptcy filings don't wait for your roadmap. Neither does an SCRA match or an OFAC hit.

Post-origination tooling decides how often a human has to touch a loan and how much that touch costs.

That's not a feature discussion. It's unit economics. And it has a right answer before you launch.

The surface is knowable. You can list what you need, decide what to build versus buy, and close the gaps while the decision is still cheap.

After launch, the same gap becomes a compliance exposure and a cost that grows with every new account.

Post-origination is where every loan lives for its entire life. The question is whether you scope the tools now, while it's still a planning decision, or later, when it isn't.

Two of these areas go deeper than this piece: compliance case management and retroactive recalculation. If that's the decision in front of you, the build-vs-buy breakdown is the next read.

lender’s priority list. But that doesn’t mean compliance is straightforward, even for lenders with the most earnest intentions. Often, legacy infrastructure is the culprit, making it difficult for lenders to take the actions clearly outlined in the law. Even regulations that haven’t changed for some time—like the—still present significant challenges for many lenders.

The SCRA grants active-duty service members the ability to request certain protections during the period of their deployment, enabling them to devote their energy to serving the country. These protections include a reduction in interest rate to a maximum of six percent on any pre-service loans. While the SCRA in its current version has been law since 2003, the number of recent enforcement actions indicates just how difficult it is for many lenders to comply with the SCRA’s interest rate protections.

Blunt tools in the absence of a scalpel

For example, in October of 2022 the Department of Justice (DOJ) announced that the financial leasing arm of GM agreed to pay over $3.5 million to resolve allegations in relation to

Peach’s approach to SCRA

At Peach, we brought real-life lending experience to the design of our platform. So from day one, we recognized the importance of being able to make retroactive changes to loans. (There are numerous applications beyond SCRA, including our Supported Portfolio Migration.) In the case of SCRA, Peach has long enabled lenders to retroactively change interest rates and waive past fees—as separate, manual actions.

Peach’s approach to SCRA

This was functional, but the ideal way to implement SCRA is to make these changes simultaneously. We now support this capability by leveraging the power of Peach's Loan Replay™ engine, which can make changes to the ledger at any time, and then recalculate a loan’s history in light of those changes. The new combined functionality is as user-friendly for your agents as processing a payment.

Peach’s approach to SCRA

Specifically, the new SCRA feature allows your agents to perform the following adjustments simultaneously on a loan of an active-duty service member:

- Lower interest rates to 6% (and lower the recurring payment during the active-duty period to account for the interest rate reduction)

- Waive fees, if necessary

- Enact these changes retroactively, if necessary, and replay the loan history with the rate and fee adjustments

- Preview the intended changes

“We launched our first product on Peach in six weeks. Eighteen months later.”

John Smith, CMO

Our SCRA functionality is available via API as well as through our white-label agent tool. The white-label agent interface can be seen here:

Peach’s approach to SCRA

Our SCRA functionality is available via API as well as through our white-label agent tool. The white-label agent interface can be seen here:

For those working directly with the API, this can be as simple as sending the following request body to the SCRA endpoint:

You’ll receive a response with either the actual post-SCRA adjusted payment plan or a preview of it. Below is a comparison of a payment plan prior to the SCRA adjustment, and the expected payments after the SCRA adjustment. The SCRA period is in effect for the first two months, and thus you will see the interest rates lowered to 6% in the response body (and the recurring amount due lowered by the amount of the interest rate reduction for the two relevant months). The origination fee has also been canceled.

The breadth of loan data needing to be adjusted means that rewriting loan histories requires the right design and abstractions, and having a built-in layer of abstraction to handle retroactive changes is the only feasible approach. Because of our team’s combined experience in the real world of lending, we know that the need to edit past loan events is inevitable. So we’ve designed a system that makes these changes as painless and automated as possible.