What Is Embedded Lending After the Loan Funds

You've priced the front door, not the house.

Embedded lending isn't just origination; it's a multi-year servicing commitment that starts the moment funds move and carries its own regulatory load from day one. If you leave that out of the model, you're understating both cost and risk. Add that column before the decision is made.

Embedded Lending Runs Longer Than the Application

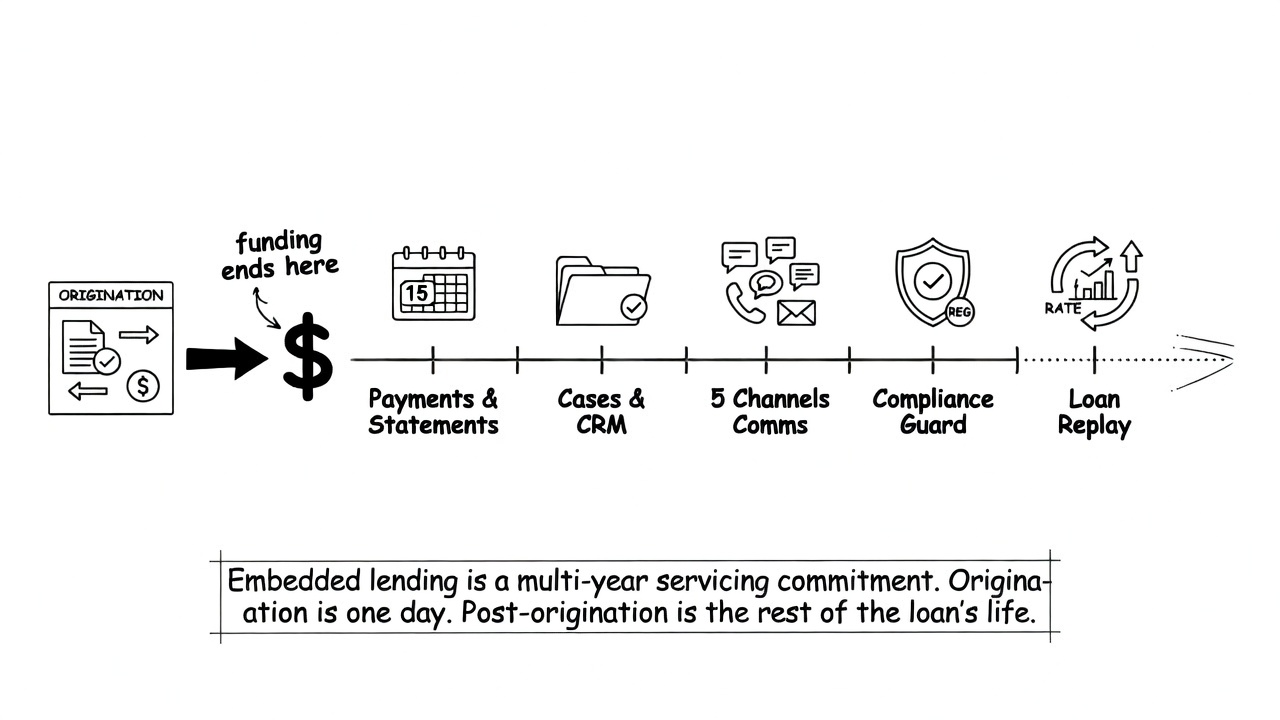

A product manager sketching the internal business case for embedded lending usually draws the same slide. Apply flow, credit decision box, disbursement. It ends at funding.

Half the operating work isn't on that slide yet.

Embedded lending means a lender or platform puts credit products directly inside a non-bank product experience, so the loan surfaces where the borrower already is. Origination covers the apply flow, decisioning, and disbursement. Early planning concentrates here because that's where the visible product work happens.

Post-origination starts the moment disbursement, KYC, and underwriting are complete. Everything after that belongs to it. Borrowers make payments. They miss them. They call with questions, file disputes, or get deployed on active military duty. Someone has to handle each of those situations, correctly, for every borrower, across the full life of every loan.

Origination is a one-time event. Servicing runs until the loan closes.

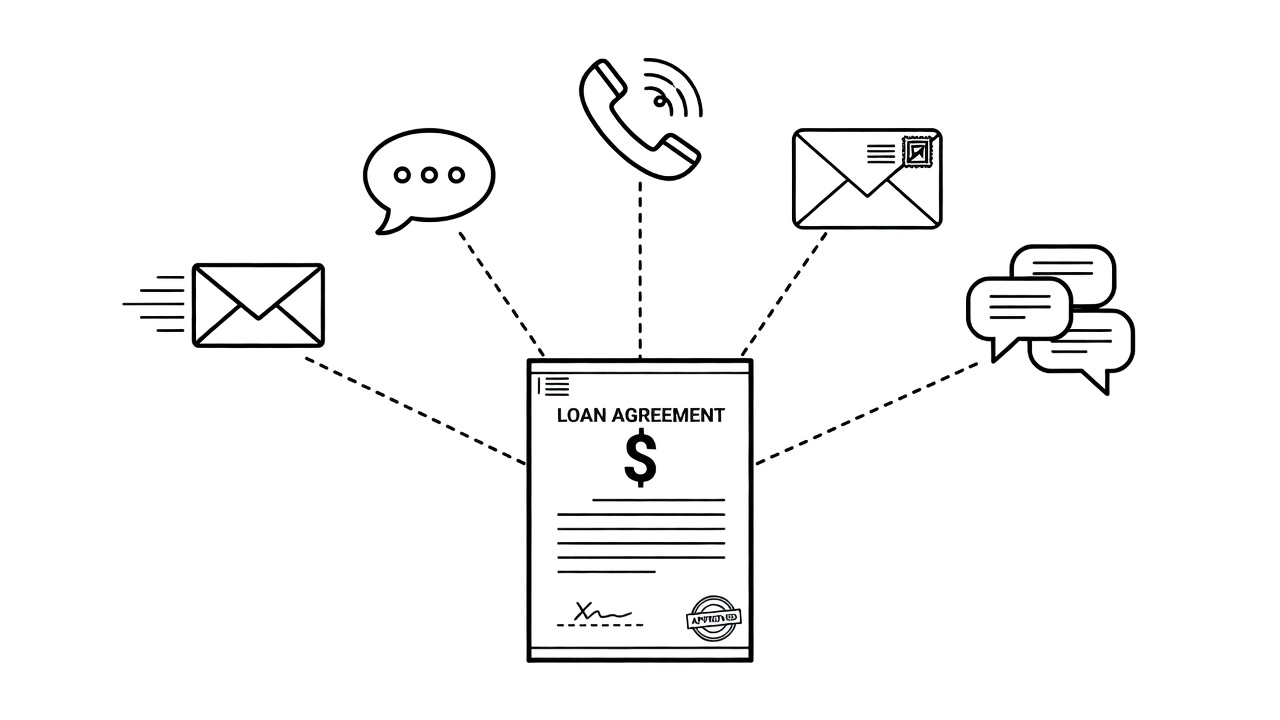

Peach's Servicing Suite covers the post-origination period end to end. Its four components are a white-labeled borrower portal, a white-labeled agent CRM, communications, and collections. Each one covers a distinct piece of what keeping a loan active requires. Borrowers need a place to log in. Agents need a workspace. Outreach needs a channel, and delinquent accounts need a collections workflow.

Servicing starts the day the first loan funds and runs until the last one closes.

What the Operating Surface Looks Like When You Are in It

Six months after launch, a collections manager pulls up a borrower record and sees a bankruptcy notification. Someone filed. The team knows a bankruptcy filing changes what they can and can't do with that account, but they're scanning the platform for a workflow that should handle it, and they're not finding one. That's the moment. The gap was always there; a regulated event just exposed it.

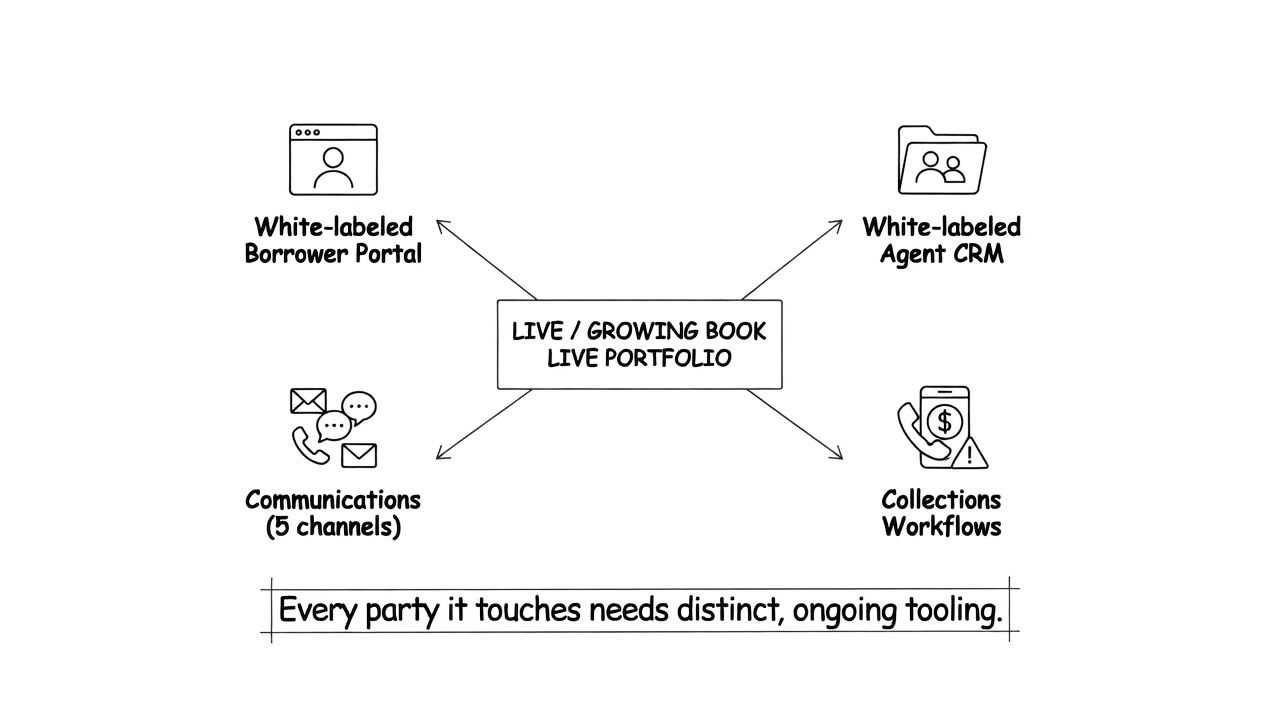

Post-origination isn't a maintenance mode. Every party it touches needs distinct, ongoing tooling. Borrowers manage their accounts through a white-labeled portal, and agents work those same accounts through a white-labeled CRM.

Communications infrastructure runs across five channels (email, SMS, phone, direct mail, and chat), with collections completing the picture. None of these are one-time configuration decisions; they're live operational systems that run against a growing book.

Running five channels without a unified platform means separate vendor relationships and separate workflows for each one. A borrower who contacts you by phone isn't automatically coordinated with the outreach your team sent by SMS two days earlier, or the case your agent opened in the CRM yesterday. Without shared infrastructure, those handoffs require manual coordination, and the operational overhead scales with every new borrower added to the book.

Peach ships handling for the regulated and operational scenarios a live portfolio generates out of the box (bankruptcy, military duty under SCRA, FEMA disasters, cease-communications orders, and others), covering the most common compliance and servicing situations a live portfolio generates. Every scenario in that set can arrive before a team has built handling for it. Without pre-built workflows, each one becomes a response assembled under live conditions.

The collections manager in that opening scenario didn't need a new build. She needed a workflow that already existed, had been tested, and was waiting for the first trigger.

Regulated case types don't announce themselves in advance. Building handling for them after the first trigger means building it while the obligation is already live, with the case sitting open and waiting.

Some events don't arrive one at a time. When a natural disaster strikes a region, it pushes many accounts into FEMA status at once. Each then requires the same accommodation. A regulatory change affecting borrowers in a particular state hits that entire cohort at once. Working through those accounts individually, case by case, isn't operationally realistic. Super Cases let a servicing team apply a single bulk action across the full affected population rather than working each account separately.

One triggered action covers everyone affected.

Volume scales with portfolio size, and it's not just regulated cases. More borrowers means more statements, more inbound contacts across all five channels, more delinquency-triggered outreach, more edge cases reaching the queue. Every account added to the book will eventually need a touchpoint, and possibly a case. A team that builds servicing infrastructure reactively (in response to growth or the first regulated event) is perpetually catching up.

Most teams that under-scope servicing don't realize it during planning. They find out when a bankruptcy notification arrives, the workflow to handle it isn't there, and someone has to figure out what to build while the clock is already running.

The Regulatory Layer That Runs Beneath Every Loan

A collections agent working a high-contact queue may not know the contact-frequency cap for every borrower's jurisdiction. Most don't. They're moving through accounts fast, applying general training, not cross-referencing state law in real time. At ten loans, that gap probably holds. At ten thousand, violations stop being a risk; they become a recurring outcome.

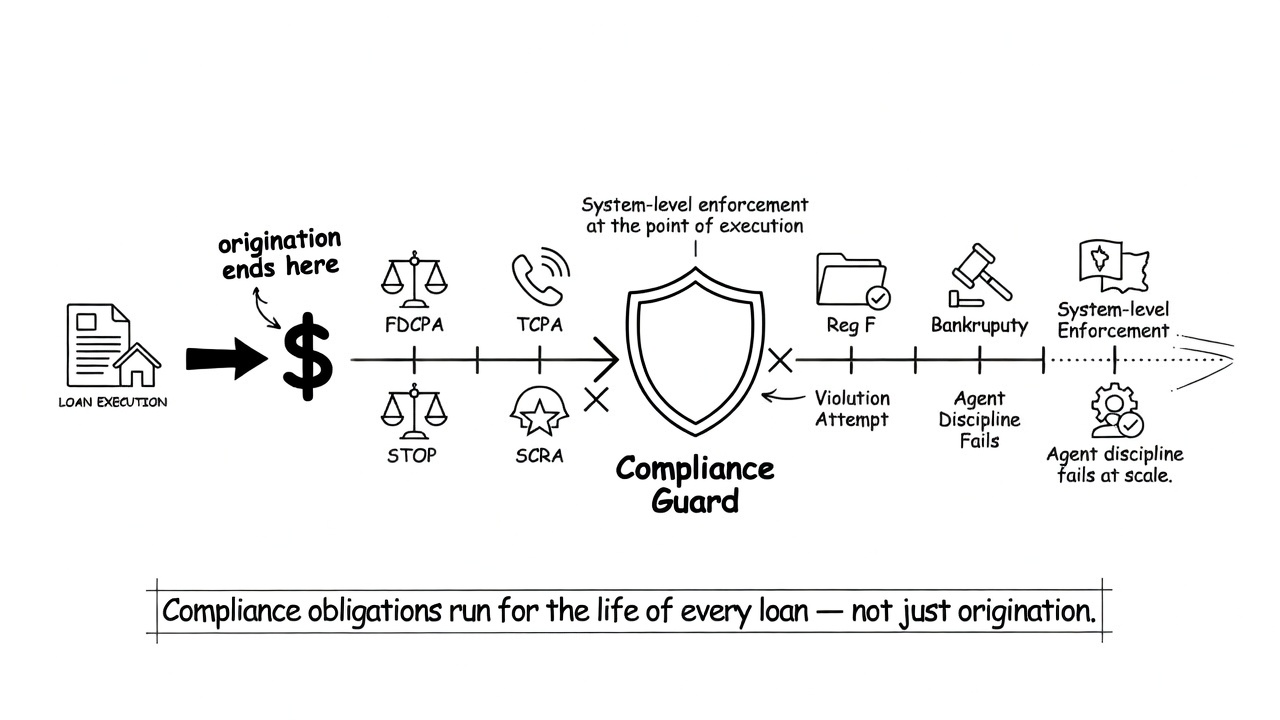

Most embedded lending plans treat compliance as an origination problem. Get the disclosures right, meet underwriting requirements, stay within credit policy. That work matters. But servicing carries its own obligations, and they run for the life of every loan. Contact frequency, bankruptcy handling, military borrower protections, debt validation. None of that belongs to origination. It runs throughout servicing, from the first payment through the last.

Several federal frameworks define that obligation set:

- The Fair Debt Collection Practices Act (FDCPA) controls how debt collectors communicate with borrowers, covering what they can say, when, and how often.

- Telephone Consumer Protection Act (TCPA) rules restrict how and when lenders can contact borrowers by phone or text.

- Federal and state prohibitions on unfair, deceptive, or abusive acts or practices (UDAP at the state level, UDAAP under federal consumer financial law) reach every borrower interaction.

- Regulation F, the CFPB's debt collection rule, adds contact-frequency limits and validation-notice requirements on top of the FDCPA baseline.

- The Bankruptcy Code governs what happens to collection activity the moment a filing appears.

When a borrower is called to active duty, the Servicemembers Civil Relief Act (SCRA) restricts collection activity. These protections aren't discretionary. Once a borrower's active-duty status is established, the lender has to honor them. Missing an active military status in a portfolio isn't a compliance edge case. Whether the lender catches the status or not, the obligation is live.

State rules compound the federal ones. Massachusetts caps collection calls at two within any seven-day window. An agent who knows the federal baseline may still violate that cap if they're not tracking the specific rules for every borrower's jurisdiction. A collections manager running a call queue on day five might not know a specific borrower is already at the cap.

The third call goes out.

The lender doesn't find out about the violation the moment it happens. They find out six weeks later when a complaint arrives. Peach's Compliance Guard changes that sequence: it checks each outbound call against the borrower's remaining interaction capacity for that window and blocks any that would exceed the cap. Agents can't override program-level rules. The Massachusetts cap isn't a policy the agent has to recall; it's a constraint the system holds.

Frequency limits are one obligation. Another involves identifying the right borrower populations fast enough to act. Compliance Guard auto-detects and creates cases when it finds active military status under SCRA, a deceased borrower, a bankruptcy filing, an OFAC or Specially Designated Nationals match, or a FEMA disaster designation. Across a live portfolio, those situations don't announce themselves. Waiting on manual identification to catch them runs the same risk as asking agents to count their own calls.

Agent discipline is a compliance model that fails at scale. System-level enforcement is the only one that doesn't.

When Servicing Data Has to Go Back in Time

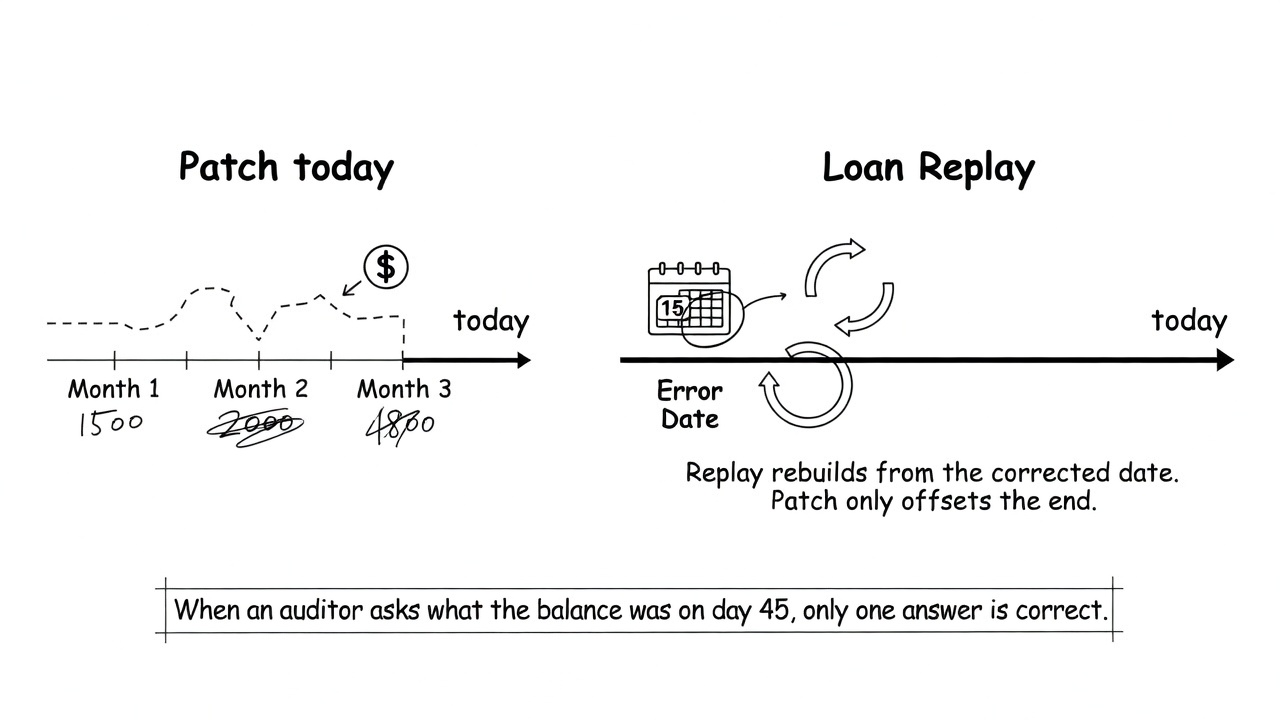

Three months in, a collections manager pulls a rate audit and finds a configuration error: a cohort of loans has been accruing interest at the wrong rate since the program launched. The error isn't the hard part. The question is where the correction has to anchor.

The instinct is to post an adjustment entry at today's date. That works for simple discrepancies, but it doesn't restate the math for the intervening period. Every balance calculation, interest accrual, and payment application that ran from the error date forward was computed on bad inputs. A today-dated correction offsets the current balance. It doesn't fix what the ledger recorded in month one, month two, or month three.

Those interim states still carry the wrong numbers.

Peach's Loan Replay handles this differently. It applies a servicing change at any past effective date and replays the entire interim period forward from that anchor point, recomputing every downstream calculation between then and now. The result is a ledger that reads as if the correction was always in place, not one that shows a wrong original path and a correction entry that brings the balance current.

Loan Replay is a recalculation engine, not a reconciliation or matching engine.

It doesn't align two sets of records or locate where they diverge. It rebuilds from the corrected starting point forward, producing a single consistent ledger state.

The difference matters most when something downstream depends on the interim period. A patched ledger and a recalculated ledger carry the same ending balance. An auditor asking what a specific loan's balance was on day forty-five gets a different answer from each one.

Changing a Live Loan Program Without Touching the Code

A program manager needs to adjust the payment grace period for a specific loan cohort. Engineering is buried, the next sprint is three weeks out, and the change needs to happen now. Does it need a code deploy, or just a configuration change?

Most servicing platforms make that distinction irrelevant by routing everything through code. Behavioral changes mean tickets, testing, and deployment risk, every time.

Peach's Adaptive Core works differently. More than 200 configuration variables control loan program behavior, and most changes to those variables go live without a code deploy. A program manager or solutions team can adjust many program behaviors through configuration alone, without touching production code or waiting on a sprint, though not every variable is changeable on a live portfolio.

"Configurable without a code deploy" and "changeable on any live portfolio" aren't the same thing, though. Some variables can be updated on an active book. Others only apply to new loan setups. A grace period adjustment might be live-mutable; a change to underlying loan term structure might not be.

Which variables fall into which category is implementation-phase work. Discovering that boundary mid-operation, after committing to a program decision, is a harder position than mapping it before launch.

Map the boundary before launch, not after.

Getting Your Loan Data Out

A regulatory report is due. Last month's full loan portfolio needs to land in Snowflake by end of week. Whether that happens on the operator's schedule or the vendor's is a question most teams don't think to ask until they're already in production.

Many servicing platforms treat data access as an export function, something you request, they produce, and you receive on their timeline. For occasional reporting, that's tolerable. For a lender carrying regulatory obligations on a defined schedule, it creates a dependency the operator can't afford.

Peach offers four data access methods. Direct API and webhooks cover real-time and event-driven data pulls. A database replica delivers to the customer's own GCS or Snowflake environment on the customer's schedule, not to a vendor-hosted location. Loan tapes round out the set.

All four are initiated by the operator, which means pulling data doesn't require opening a support ticket or waiting on a vendor-side export queue.

Regulators don't adjust their deadlines because a vendor's export queue ran long. Embedded lenders carry reporting obligations on fixed timelines, and an analyst waiting on a vendor-side export to meet one of them has already lost control of the process.

Embedded Lending Is a Multi-Year Operating Commitment

A CTO building the final evaluation slide for an embedded lending program has columns for product, origination infrastructure, unit economics, and distribution. Servicing usually isn't one of them.

The gap matters before the decision is made. Origination is the visible side, covering the product you're building, the rails you're standing up, and the market you're going after. Servicing starts the day the first loan funds and runs until the last one closes.

The compliance obligation doesn't wait for the servicing build to catch up. Between the decision to launch and the first borrower who needs a bankruptcy case opened, a cease-communications request honored, or a dispute handled inside a regulatory window, there's no grace period. Those cases arrive on whatever schedule life produces for your borrowers. A lender that funds loans before the servicing layer is in place is already behind.

That's the tiebreaker question the evaluation slide doesn't show. Not whether to build or buy, but whether the servicing plan exists before the first disbursement. Organizations that scope origination thoroughly and treat servicing as a second-phase problem routinely find the second problem harder than the first. The regulatory surface is wider, the edge cases are more varied, and the cost of a missed case isn't a bad user experience.

It's a regulatory action.

Peach staffs implementation with Solutions engineers, not a scripted help desk. At go-live, the question isn't how to use a feature. It's how to configure the system correctly for a specific portfolio.

Add the servicing column.

lender’s priority list. But that doesn’t mean compliance is straightforward, even for lenders with the most earnest intentions. Often, legacy infrastructure is the culprit, making it difficult for lenders to take the actions clearly outlined in the law. Even regulations that haven’t changed for some time—like the—still present significant challenges for many lenders.

The SCRA grants active-duty service members the ability to request certain protections during the period of their deployment, enabling them to devote their energy to serving the country. These protections include a reduction in interest rate to a maximum of six percent on any pre-service loans. While the SCRA in its current version has been law since 2003, the number of recent enforcement actions indicates just how difficult it is for many lenders to comply with the SCRA’s interest rate protections.

Blunt tools in the absence of a scalpel

For example, in October of 2022 the Department of Justice (DOJ) announced that the financial leasing arm of GM agreed to pay over $3.5 million to resolve allegations in relation to

Peach’s approach to SCRA

At Peach, we brought real-life lending experience to the design of our platform. So from day one, we recognized the importance of being able to make retroactive changes to loans. (There are numerous applications beyond SCRA, including our Supported Portfolio Migration.) In the case of SCRA, Peach has long enabled lenders to retroactively change interest rates and waive past fees—as separate, manual actions.

Peach’s approach to SCRA

This was functional, but the ideal way to implement SCRA is to make these changes simultaneously. We now support this capability by leveraging the power of Peach's Loan Replay™ engine, which can make changes to the ledger at any time, and then recalculate a loan’s history in light of those changes. The new combined functionality is as user-friendly for your agents as processing a payment.

Peach’s approach to SCRA

Specifically, the new SCRA feature allows your agents to perform the following adjustments simultaneously on a loan of an active-duty service member:

- Lower interest rates to 6% (and lower the recurring payment during the active-duty period to account for the interest rate reduction)

- Waive fees, if necessary

- Enact these changes retroactively, if necessary, and replay the loan history with the rate and fee adjustments

- Preview the intended changes

“We launched our first product on Peach in six weeks. Eighteen months later.”

John Smith, CMO

Our SCRA functionality is available via API as well as through our white-label agent tool. The white-label agent interface can be seen here:

Peach’s approach to SCRA

Our SCRA functionality is available via API as well as through our white-label agent tool. The white-label agent interface can be seen here:

For those working directly with the API, this can be as simple as sending the following request body to the SCRA endpoint:

You’ll receive a response with either the actual post-SCRA adjusted payment plan or a preview of it. Below is a comparison of a payment plan prior to the SCRA adjustment, and the expected payments after the SCRA adjustment. The SCRA period is in effect for the first two months, and thus you will see the interest rates lowered to 6% in the response body (and the recurring amount due lowered by the amount of the interest rate reduction for the two relevant months). The origination fee has also been canceled.

The breadth of loan data needing to be adjusted means that rewriting loan histories requires the right design and abstractions, and having a built-in layer of abstraction to handle retroactive changes is the only feasible approach. Because of our team’s combined experience in the real world of lending, we know that the need to edit past loan events is inevitable. So we’ve designed a system that makes these changes as painless and automated as possible.