How to Choose a Loan Management System Before the Demo Misleads You

You've priced the migration. You haven't priced what breaks eighteen months after go-live. Your evaluation is probably measuring demo performance, not operational failure modes. Still deciding whether to build or buy loan management software? Settle that first. Everything below assumes you're buying. The six questions here surface the difference between a vendor who has run into real lending edge cases and one who is still describing the slide.

The Checklist Won't Tell You What Breaks After Launch

The spreadsheet has four vendors across the top and about thirty rows down the left side. Origination integration. Configurable loan types. API availability. Payment processing. Every row gets a checkmark or a gap, and the vendor with the fewest gaps wins the shortlist.

Nothing in those columns tests what happens when a fee case breaks at volume.

Nothing tests whether a modification loses its status trail when two conditions hit at once, or what the system does when lending is live and the load is real.

The guidance you'll find on choosing a loan management system reads as a feature checklist, and that's the wrong way to choose.

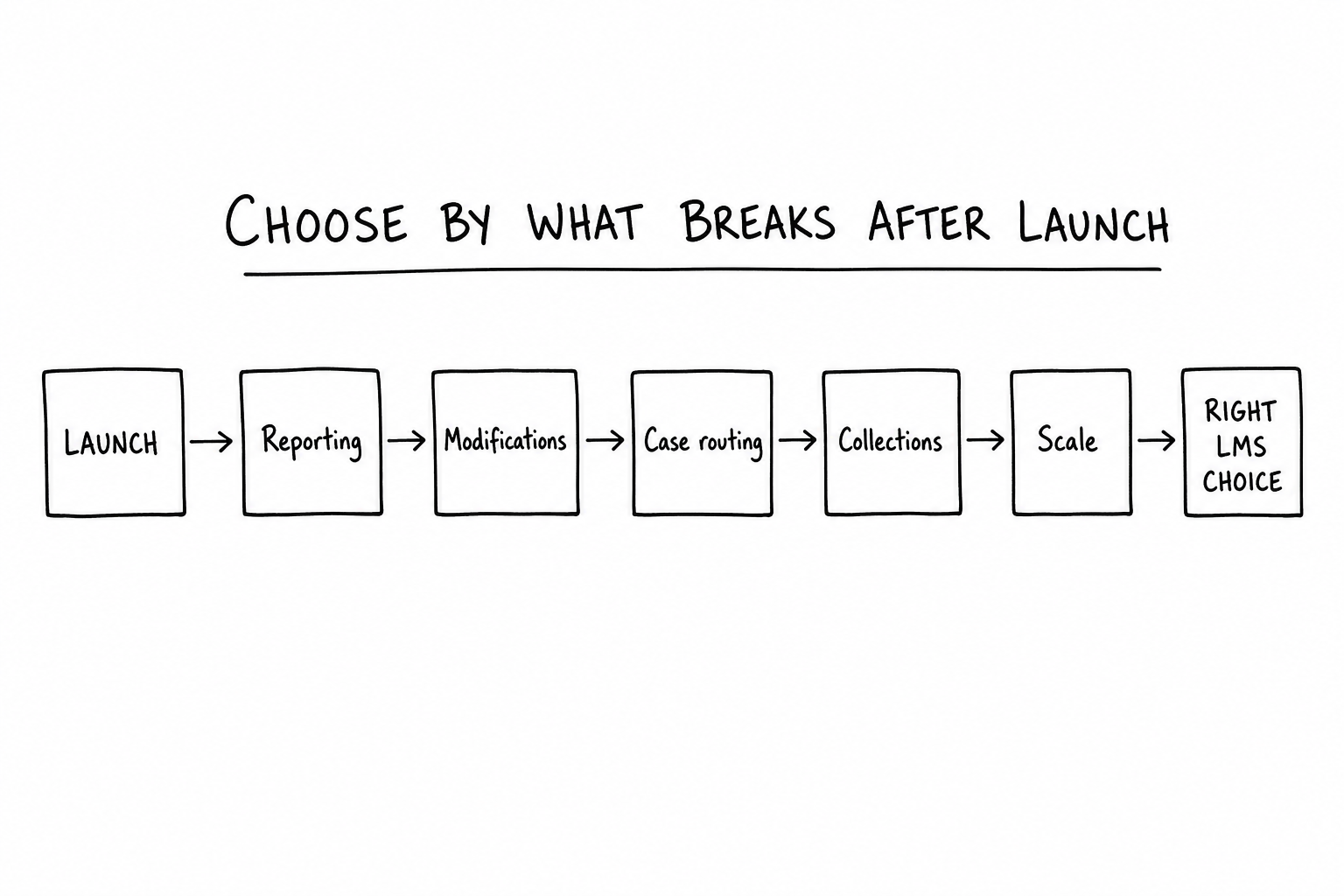

The right frame is failure-mode evaluation. Test whether the system holds up in the operational scenarios that will decide if the purchase was right, not whether the demo was well-prepared. A system that handles a demo cleanly can still break on the edge cases that hit your servicing team every week.

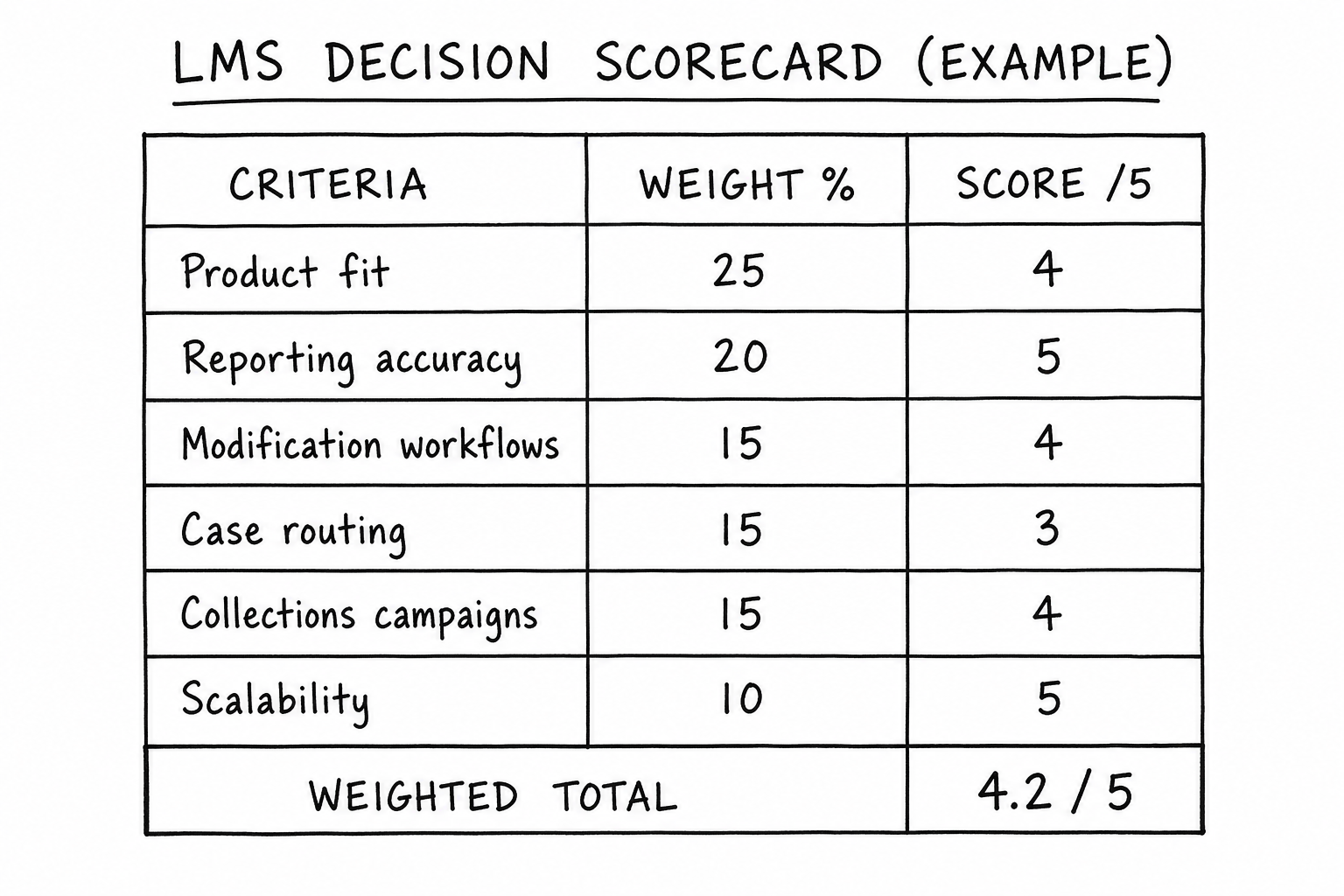

Post-launch, a different set of questions decides it. Can the system support your product structure, including the fees, the interest calculations, and the edge cases specific to your product? Does it produce accurate reporting? Handle loan modifications correctly? Route and escalate cases? Support early collections work? Does it hold up as loan volume grows?

Each of those is a category of operational risk your servicing team carries after go-live.

None of them appears as a checklist row.

Checklists feel convincing because they're legible. A spreadsheet with forty rows and four vendors gives you something to compare. It compares the wrong thing.

A checklist tells you which features a vendor was willing to claim in a sales process. But it describes what a demo environment was built to show well. A production system running your actual loan volume is a different test entirely.

The next decision is which failure modes your product will produce and whether the system can handle them, not which features to count.

Already Running Demos? You're Probably Measuring the Wrong Things

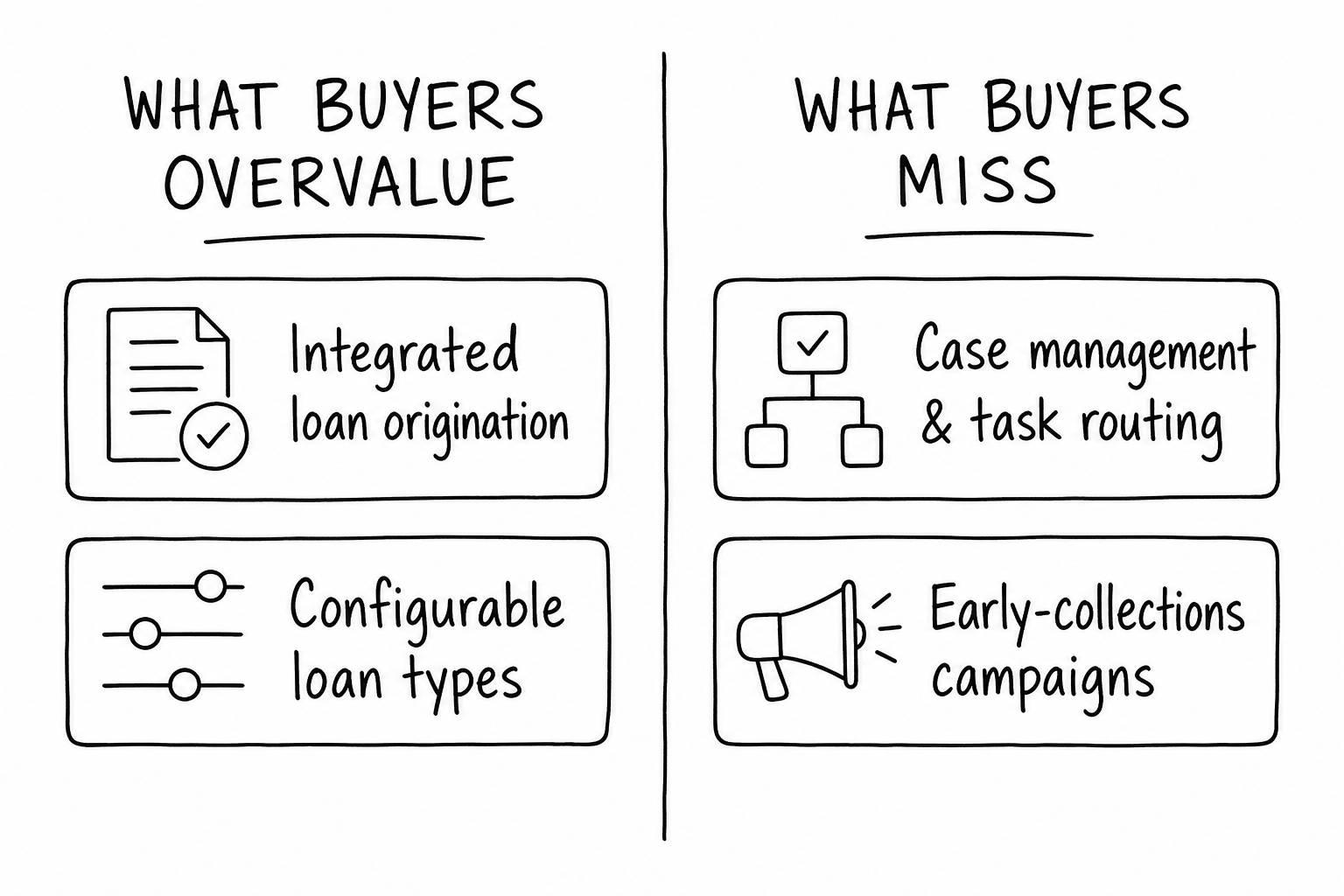

Four demos in, your comparison matrix probably has origination workflow and configurable product types in the top two rows. Those are the features most vendors lead with. They're also the two that matter least for what happens after the first loan books.

Start with origination. Origination is a distinct stage from servicing, and an LMS runs servicing across the full loan life, not just the origination moment. The application-to-booking handoff tells you almost nothing about what happens two years in.

Configurable loan types carry the same misdirection. A system that lets you define your product doesn't prove it can run that product correctly over the full loan lifecycle.

Configurability is a starting point, not a proof.

A vendor demo shows you a clean path through a single expected scenario. What you need to know is what happens at the edge of that scenario. A fee structure that doesn't fit the template. A modification that conflicts with a pending collections action.

Two criteria that rarely show up in a comparison matrix are the ones that decide operational health after launch.

Case management and task routing is what keeps servicing work organized, escalated, and handled correctly once loans are live. A system without it relies on people to catch what the platform should be routing automatically. The case types behind that work, and how a platform detects and routes them, are mapped in the tools a lender needs after a loan starts.

Campaign capability for early-stage collections is where a lender protects portfolio performance before accounts deteriorate. Miss this in an evaluation, and you're running governance by workaround once accounts age.

Criterion One: Can the System Actually Run Your Loan Product?

"We support buy-now-pay-later." An account executive says it in the second slide.

That's probably true. It tells you almost nothing about what the system will do with your product.

Supporting a loan category and running a specific product are different answers to different questions. Category support is easy to claim. What matters after launch is whether the system handles the fee structures, interest calculation methods, modification scenarios, and edge cases specific to your product.

Product-structure fit isn't the loan type checked in a feature grid. It's whether the system can carry your specific product without engineering work every time a non-standard case comes in.

Ask which fee, interest, modification, and exception cases the system handles natively versus which require custom development.

Natively means the system runs it without someone writing code.

A configuration wrapper that has to be extended each time a non-standard case appears looks the same in a demo and costs more every week after go-live.

A system that requires workarounds for product-specific edge cases doesn't stop requiring them. Those workarounds become operational cost the team carries indefinitely.

Fees aren't just a ledger entry. A servicing platform needs to control how product-specific fees are applied, how insurance products interact with loan balances, and how remediation gets tracked when something goes wrong.

Fee administration is where regulators have acted: in 2018, the CFPB addressed Wells Fargo over auto-loan insurance administration and mortgage rate-lock extension fee charges.

So the question to bring into your next demo isn't whether they support your loan type. It's whether they can walk you through a non-standard case in your product and show how the system handles it without custom work.

Criterion Two: Will a Regulator Trust the Reports?

Two quarters after go-live, an auditor asks your ops team for a corrected payment history report. The system can pull the original. It can't flag what's wrong with it, produce a corrected version, or leave a trail showing what changed and why.

That's the moment reporting quality becomes a criterion and not a given.

Every LMS generates reports. The evaluation question is different: how does the system validate those reports, correct errors when they surface, and produce an audit record showing the work was done? Those are three distinct capabilities, and most demos don't surface them.

Clear, thorough, and accurate data reporting is a standalone selection criterion because it's what the business, auditors, and regulators rely on after launch, not during it. The system that services the loan has to stand behind the data years later, when someone pulls a report under examination conditions.

A 2017 CFPB enforcement action against Nationstar Mortgage shows what's at stake. The action arose from flawed mortgage-loan reporting, and the outcome required Nationstar to pay a civil penalty and correct its reporting data. The lesson for system selection: a servicing platform needs to support not only accurate initial reporting but also the workflow for catching errors after they occur and producing documentation of the correction.

And CFPB examiners haven't stopped finding the same category of problem: the Summer 2024 Supervisory Highlights documented continued servicing and debt-collection violations.

The regulator sees the data either way. What the exam tests is your correction workflow: a built-in process for flagging errors, generating corrected outputs, and leaving a record of what changed. If the system can't do that, your ops team is building it manually while the clock runs.

Ask your vendor to show you the correction and audit workflow, not a report. Whether the report generates isn't the question anymore.

Criterion Three: Does the System Stop the Wrong Thing From Happening?

A borrower calls to request a payment deferral. A modification is already under review. The collections system checks its queue, sees no open case flag, and fires the first outreach sequence. No hold blocks it. The system has recorded the case status. It just doesn't use that record to stop what happens next.

This criterion tests whether the system acts on what it records.

When a borrower asks for relief, a servicer runs loss mitigation, the process of evaluating that request before any enforcement action moves forward. While that evaluation is open, the system has to handle loan modifications with clear status tracking, borrower notices, and foreclosure holds. A foreclosure hold is a system-enforced pause that prevents an irreversible action from proceeding until all required conditions are met. Same logic applies to any downstream action that can't be undone. The hold runs while the case is open, not after the action has already fired.

Regulators have sanctioned servicers for getting this wrong.

In 2017, the CFPB found that Fay Servicing had advanced toward foreclosure while borrowers still had relief requests pending. The failures regulators cited map to status tracking, borrower notices, and holds. A 2020 consent order against Specialized Loan Servicing sharpened the finding. The CFPB concluded the servicer had taken prohibited foreclosure actions against borrowers entitled to protections and had failed to send required evaluation notices on time.

In both cases, the workflow didn't stop the wrong step before it ran.

Ask your vendor how the system routes, escalates, and freezes work when a case requires it. The answer reveals whether status holds the next step or records what already ran.

Collections Governance and Scale: The Two Criteria Buyers Leave Until the End

Fifty thousand active loans in the portfolio. Automated outreach running. And somewhere in the operations team, someone is figuring out that the system has been contacting borrowers whose accounts were flagged for a payment plan, because the suppression logic that would have blocked those contacts was never built. The system automates but doesn't govern.

Early-stage collections is where a lender protects performance before accounts deteriorate and loss becomes harder to prevent. Getting there early matters. But automation is only the outbound mechanism. Whether those contacts are appropriate depends on configurable suppression rules that keep certain accounts off the list, audit trails that show which accounts were contacted and why, and override controls that let your team freeze a campaign when something goes wrong.

Without those, automation doesn't improve compliance outcomes. It sends the wrong contacts out faster.

In 2015, the CFPB and the FTC brought a joint action against Green Tree Servicing over servicing and collection practices that harmed borrowers. The enforcement record didn't establish automation as the problem. Collection practices without adequate governance caused harm at scale, and that's the evaluation question. Not whether the system automates outreach, but whether a lender can configure what that automation does and doesn't reach.

CFPB examiners continued finding servicing and debt-collection violations in the agency's Summer 2024 Supervisory Highlights. Not historical precedent. Current findings.

Your system handles today's volume. What happens when the portfolio climbs isn't a question you can defer. Platform performance under real and growing loan volume is its own criterion. How the system behaves at scale gets decided the day you select it, not the day you hit the volume.

Ask your vendor what breaks first as loan volume grows, and require specifics. A vague answer signals the platform hasn't been stress-tested at the volume you're heading toward.

Both criteria, collections governance and scale, show up after the contract is signed, not during the demo.

Six Questions to Ask Every Vendor, and What an Honest Answer Looks Like

When a vendor tells you their system supports "virtually any loan product," you're not receiving a feature claim. They're avoiding your most important question.

Ask it anyway. Which lending products isn't this system built for?

A vendor who answers with precision is signaling the same operational discipline the evaluation criteria test for in the platform itself. One who claims universal fit is telling you something too.

Six questions reveal real capability versus marketed capability.

- Which fee, interest, modification, and exception cases does the system handle natively, and which require custom development?

- How are reports validated, corrected, and audited, not just generated?

- How does the system route, escalate, and freeze work when a case requires it?

- How are early-collections campaigns governed, suppressed, and kept compliant?

- What breaks first as loan volume grows, and what's a specific example?

- Which lending products isn't this system built for?

Each question maps to a failure mode the prior sections named. The answers tell you whether the vendor has run into those failure modes or is still describing the demo.

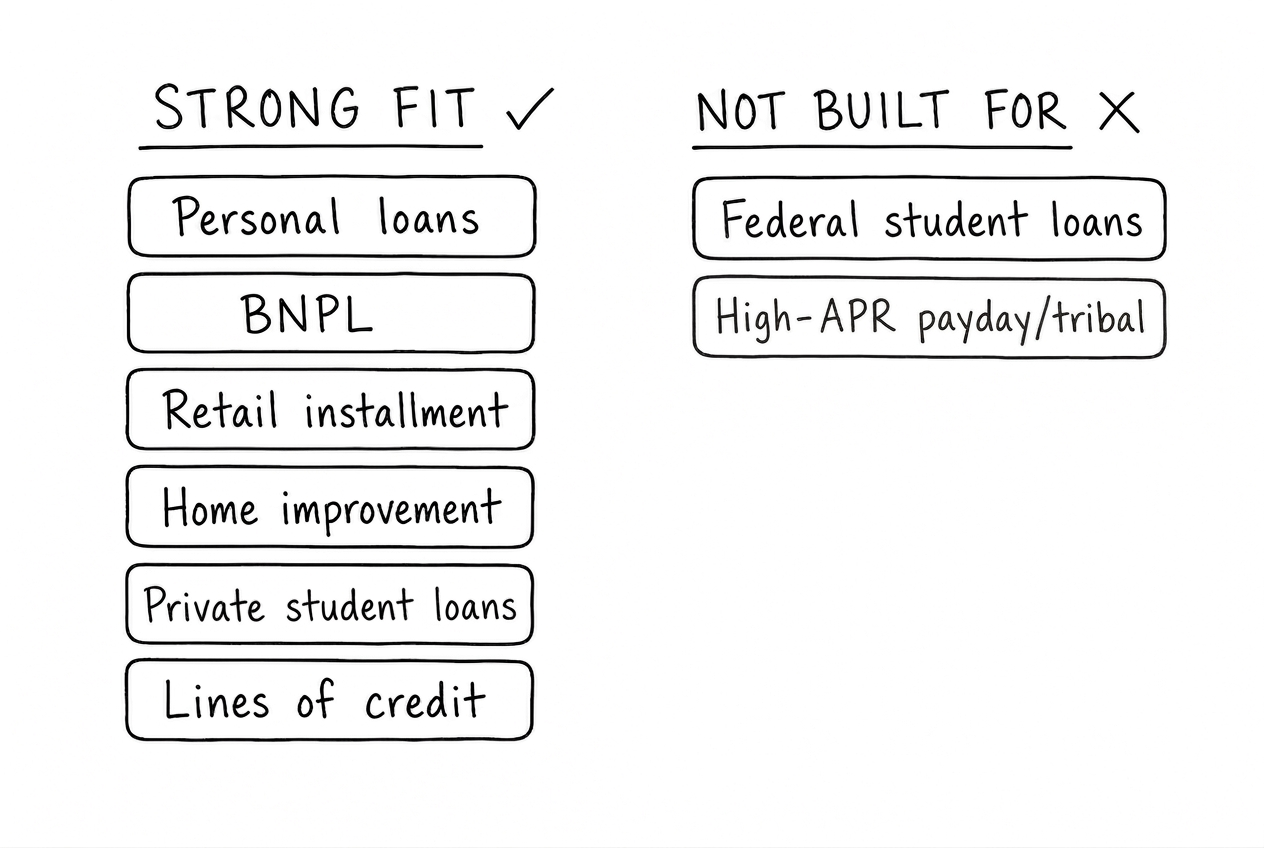

Peach is a strong fit for installment lending, including personal loans, buy-now-pay-later, retail installment contracts, home improvement loans, private student loans, and single-term cash advances. It's a strong fit for card and revolving credit, including unsecured and secured credit cards, charge cards, virtual cards, and business lines of credit. And it's a strong fit for business lending, including secured and unsecured business loans, business credit, and invoice financing or factoring.

On non-fit, the answer is equally specific. Federal student loans are the only hard technical no. Payday and tribal lending models built around very high APRs are also outside the fit. Private student loans are supported. Mortgage, auto, and leasing programs aren't currently offered as such, and a lender whose core product is in those markets is usually a better fit elsewhere.

You're looking for that. Specific. Bounded. Not padded.

A vendor who can name what they don't do (precisely, not evasively) has already passed the test the sixth question was designed to run.

lender’s priority list. But that doesn’t mean compliance is straightforward, even for lenders with the most earnest intentions. Often, legacy infrastructure is the culprit, making it difficult for lenders to take the actions clearly outlined in the law. Even regulations that haven’t changed for some time—like the—still present significant challenges for many lenders.

The SCRA grants active-duty service members the ability to request certain protections during the period of their deployment, enabling them to devote their energy to serving the country. These protections include a reduction in interest rate to a maximum of six percent on any pre-service loans. While the SCRA in its current version has been law since 2003, the number of recent enforcement actions indicates just how difficult it is for many lenders to comply with the SCRA’s interest rate protections.

Blunt tools in the absence of a scalpel

For example, in October of 2022 the Department of Justice (DOJ) announced that the financial leasing arm of GM agreed to pay over $3.5 million to resolve allegations in relation to

Peach’s approach to SCRA

At Peach, we brought real-life lending experience to the design of our platform. So from day one, we recognized the importance of being able to make retroactive changes to loans. (There are numerous applications beyond SCRA, including our Supported Portfolio Migration.) In the case of SCRA, Peach has long enabled lenders to retroactively change interest rates and waive past fees—as separate, manual actions.

Peach’s approach to SCRA

This was functional, but the ideal way to implement SCRA is to make these changes simultaneously. We now support this capability by leveraging the power of Peach's Loan Replay™ engine, which can make changes to the ledger at any time, and then recalculate a loan’s history in light of those changes. The new combined functionality is as user-friendly for your agents as processing a payment.

Peach’s approach to SCRA

Specifically, the new SCRA feature allows your agents to perform the following adjustments simultaneously on a loan of an active-duty service member:

- Lower interest rates to 6% (and lower the recurring payment during the active-duty period to account for the interest rate reduction)

- Waive fees, if necessary

- Enact these changes retroactively, if necessary, and replay the loan history with the rate and fee adjustments

- Preview the intended changes

“We launched our first product on Peach in six weeks. Eighteen months later.”

John Smith, CMO

Our SCRA functionality is available via API as well as through our white-label agent tool. The white-label agent interface can be seen here:

Peach’s approach to SCRA

Our SCRA functionality is available via API as well as through our white-label agent tool. The white-label agent interface can be seen here:

For those working directly with the API, this can be as simple as sending the following request body to the SCRA endpoint:

You’ll receive a response with either the actual post-SCRA adjusted payment plan or a preview of it. Below is a comparison of a payment plan prior to the SCRA adjustment, and the expected payments after the SCRA adjustment. The SCRA period is in effect for the first two months, and thus you will see the interest rates lowered to 6% in the response body (and the recurring amount due lowered by the amount of the interest rate reduction for the two relevant months). The origination fee has also been canceled.

The breadth of loan data needing to be adjusted means that rewriting loan histories requires the right design and abstractions, and having a built-in layer of abstraction to handle retroactive changes is the only feasible approach. Because of our team’s combined experience in the real world of lending, we know that the need to edit past loan events is inevitable. So we’ve designed a system that makes these changes as painless and automated as possible.